This is Part 2 of a 6-part series called “The New Frontier.” Part 1 laid out the vision: industrial orbit, a permanent Moon base, and the road to Mars. This article gets granular. Dates, numbers, dependencies — and where the whole thing could fall apart.

Every roadmap is wrong. The question is whether it’s wrong in useful ways.

What follows is my best attempt at a realistic, multi-track timeline for space industrialization from now through 2060. I’ve organized it in four phases, and within each phase I cover all the major tracks in parallel — Starship, Artemis, orbital compute, Mars, commercial ventures, China — because that’s how reality works. These programs don’t exist in silos. A slip in Starship affects Artemis. A breakthrough in ISRU changes the Mars calculus. China’s pace changes everyone’s funding.

For every claim, I’ll flag whether it’s confirmed (hardware built, mission flown), targeted (official schedule from the organization involved), projected (reasonable extrapolation from current trends), or speculative (my read of where things are heading, with significant uncertainty). If I think a timeline will slip, I’ll say so and explain why.

Let’s build the roadmap.

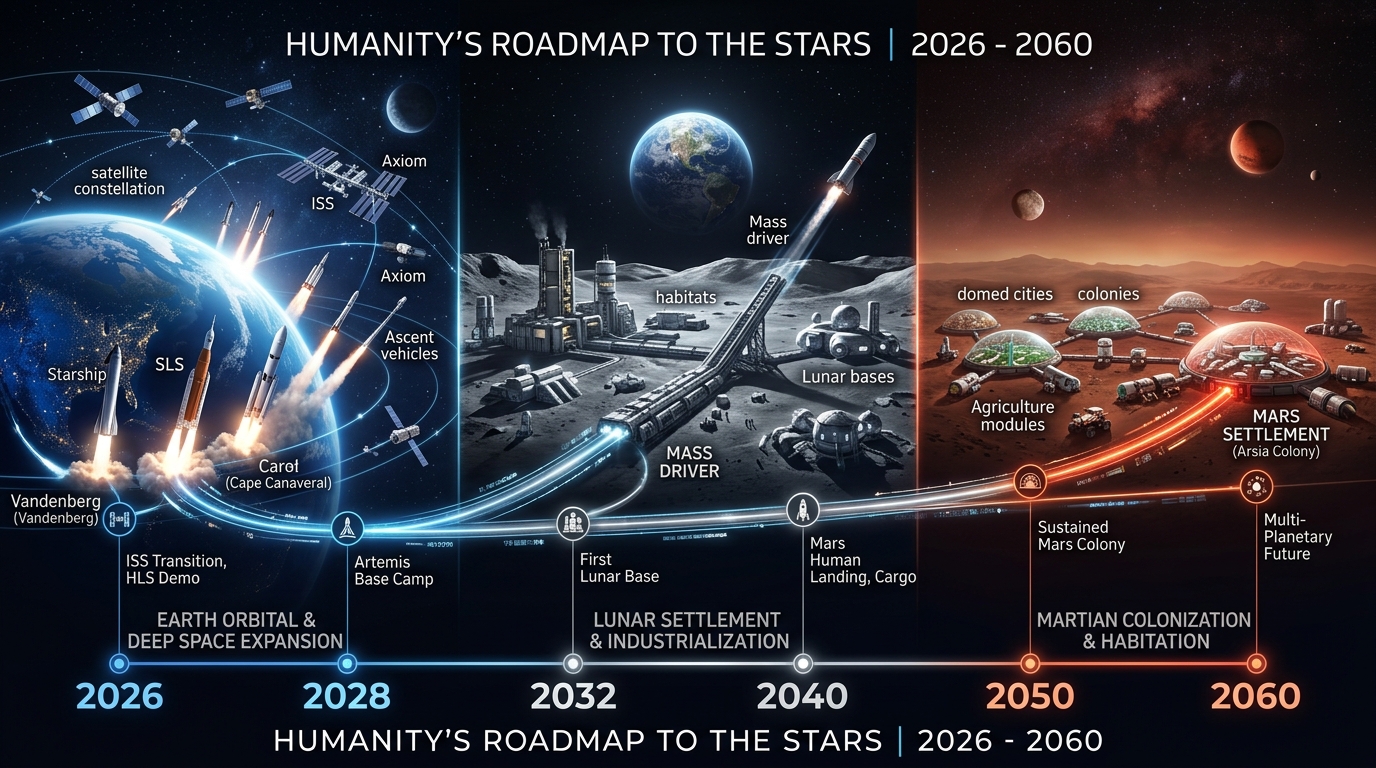

Phase 1: 2026–2028 — Foundations

This is where we are right now. The foundations are being poured — some literally, some regulatory, some in orbit. The next 30 months will determine whether the space economy accelerates or stalls for another decade.

Starship: The V3 Era Begins

Confirmed: Ship 39 completed cryogenic proof testing in March 2026. Raptor 3 engines are through qualification. Pad 2 at Boca Chica is activated and operational. The Falcon 9 drone ship Just Read the Instructions has been reassigned from Falcon recovery to Starship maritime operations — a quiet signal that SpaceX considers Starship cadence imminent.

UPDATE (May 2026): Starship V3 is no longer “targeted” — it’s on the pad. The milestones came fast:

- May 7: Full-duration, full-thrust static fire of Super Heavy V3 booster — all 33 Raptor 3 engines.

- May 9: Starship V3 Ship and Super Heavy fully stacked at Starbase for the first time — the tallest rocket ever assembled.

- May 11: Launch rehearsal completed. Over 5,000 metric tonnes of propellant loaded during a flight-like countdown.

- May 21 (targeted): IFT-12 — the first flight of Starship V3. Goals: demonstrate V3 vehicles and Raptor 3 engines, deploy Starlink simulators, test in-space Raptor relight, evaluate next-gen heat shield, and attempt offshore Super Heavy splashdown.

V3 is not a minor revision. It’s a stretched vehicle with Raptor 3 engines delivering higher thrust and specific impulse, larger propellant tanks, and catch-ready booster hardware from day one. The performance target is ~150 tonnes to LEO, fully reusable, at a cost of $100–200/kg. Musk noted the production pipeline is full: roughly 10 more ships and ~5 boosters planned for 2026. A setback on Flight 12 (unless it damages the launch stand) won’t cause major delays.

For context: Falcon 9 puts ~22.8 tonnes to LEO at roughly $2,700/kg. Starship V3, if it hits targets, represents a 13–27× cost reduction on a vehicle that carries 6.5× more payload. It’s a huge change.

Projected: If V3 flight testing goes well through mid-2026, Starlink V3 satellite deployment begins in earnest by late 2026. Each Starship launch carries 25–50× the bandwidth of a Falcon 9 Starlink mission. SpaceX is targeting a 100× increase in launch rate and deploying ~20,000 Starlink satellites per year — up from ~2,000/year on Falcon 9. This is the economic engine that funds everything else.

My honest assessment: V3 is moving faster than I expected when I first drafted this article in April. The fact that it’s already stacked, fueled, and targeting a launch date suggests SpaceX’s development cadence is accelerating, not plateauing. The cost targets ($100–200/kg) are achievable at marginal cost once reuse is proven, but the fully loaded cost, including development amortization, will be higher in the early years. Real $100/kg pricing for external customers is more like 2029–2030.

Artemis: Humans Beyond LEO Again

Confirmed: Artemis II launched April 1, 2026 and splashed down April 10, 2026. Four astronauts flew a free-return trajectory around the Moon — the first humans past low Earth orbit since Apollo 17 in December 1972. That’s a 53-year gap. The mission validated Orion’s life support, heat shield at lunar-return velocities (~11 km/s), and deep-space navigation. It worked.

Confirmed: NASA cancelled the Lunar Gateway in March 2026, redirecting approximately $20 billion toward surface infrastructure. This is a major strategic pivot — from an orbital waystation to a direct-to-surface architecture. The political subtext: Gateway was always more about international partnership than engineering necessity. The new priority is boots on regolith, fast.

Targeted: Artemis III in mid-2027 is planned as a LEO rendezvous and docking test — crew meets the SpaceX Starship Human Landing System (HLS) and Blue Origin’s Blue Moon lander in orbit. No lunar landing. Think Apollo 9: proving the vehicles work together before committing to the surface. This mission will validate orbital refueling, crew transfer, and lander systems. UPDATE (May 2026): The SLS core stage for Artemis III has begun shipping to Kennedy Space Center, and a full-scale Blue Moon Mark 2 landing cabin prototype has arrived at NASA JSC for crew training and evaluation. NASA Administrator Isaacman confirmed increased confidence in the 2027 target, with Artemis IV protecting for up to two landing attempts if needed. Astronaut selection for Artemis III is expected in the coming weeks.

Targeted: Artemis IV in early 2028 is the big one — the first crewed lunar landing since 1972, targeting the lunar south pole. Phase 1 of Moon Base begins: habitat precursors deployed, initial ISRU (In-Situ Resource Utilization) testing with water ice extraction from permanently shadowed craters.

Targeted: Artemis V in late 2028 — a second crewed landing in the same calendar year. Foundational base construction begins. Nuclear power system precursors (likely a Kilopower-class fission reactor, ~10 kW) are delivered. The goal is to move from annual SLS cadence toward monthly lander cadence post-2028, enabled by Starship HLS and commercial landers.

My honest assessment: Artemis III in mid-2027 is plausible if Starship HLS orbital refueling demos happen on schedule — which depends on V3 reliability. Artemis IV in early 2028 has maybe 50% chance of hitting that date; I’d bet on late 2028 for the first landing. Artemis V in the same year as IV is ambitious. The SLS production line is the bottleneck — there’s exactly one rocket per mission, and each takes over a year to build. NASA knows this, which is why Starship and Blue Moon as independent landers matter so much.

Orbital Compute: The Race for Space-Based AI

Confirmed: On January 30, 2026, SpaceX filed with the FCC for authorization to deploy up to 1 million satellites for AI compute infrastructure. Not Starlink internet satellites. Dedicated compute nodes in orbit.

Confirmed: TERAFAB — the orbital compute manufacturing initiative — was announced on March 21, 2026. Intel joined as a partner on April 7. The concept: build radiation-hardened NPUs (neural processing units) optimized for space, manufacture them in volume, and deploy them on satellite buses at Starship scale.

Confirmed: Blue Origin filed Project Sunrise on March 19, 2026 — a constellation of 51,600 satellites for orbital compute. Jeff Bezos is not sitting this one out.

Targeted: The first orbital AI server prototype is expected in spring 2027. This will be a proof-of-concept: a small cluster of NPUs on a satellite bus, connected via Starlink mesh, running inference workloads.

In progress: Amazon/Kuiper has filed regulatory petitions seeking to block or delay SpaceX’s 1M-satellite authorization, citing spectrum interference and orbital debris concerns. This is going to be a multi-year regulatory battle. The FCC, ITU, and possibly Congress will all be involved.

Why this matters: Earth-based AI compute is hitting power constraints. A single large AI training cluster consumes 100–500 MW. The US grid is already struggling to site new data centers. In orbit, solar flux is ~1,361 W/m², uninterrupted, no weather, no permitting fights. The physics favor space. The economics depend entirely on launch cost, which is why Starship V3 is the enabling technology.

China: The Parallel Track

Confirmed: China’s ILRS (International Lunar Research Station) construction phase runs 2026–2032, in partnership with Russia. Robotic precursor missions are underway — landers, rovers, and infrastructure testbeds deploying to the lunar south pole.

In development: The Long March-10 rocket, China’s answer to SLS, is being built for crewed lunar missions. It’s a ~90-tonne to LEO vehicle, roughly comparable to SLS Block 1.

Projected: China is targeting a crewed lunar landing by 2030. Their track record on space program timelines is actually better than NASA’s — they tend to deliver on or ahead of schedule. I’d give this a 60–70% probability of hitting 2030.

The geopolitical angle: China’s lunar program is a strategic motivator for Western space funding. Every time CNSA hits a milestone, Congressional appropriations for Artemis get a little easier to pass. This is the new space race, and it’s real.

Commercial & ISRU: The Economic Seeds

The commercial space ecosystem is planting seeds that won’t bear fruit for years, but they matter:

- SpaceCHIPs: Radiation-hardened chip designs optimized for space NPU workloads. Traditional space-rated electronics cost 10–100× as much as their terrestrial equivalents. SpaceCHIPs aims to close that gap using commercial fab processes with targeted hardening.

- Interlune: Pilot-scale helium-3 mining operation, targeting processing of 100+ tonnes of regolith per hour. He-3 is valuable for fusion research at ~$1.4 million/kg on Earth. Even small quantities justify the mission economics.

- LiftPort Group: Conducting tether deployment tests for a lunar space elevator concept. Unlike an Earth elevator (which requires materials that don’t exist), a lunar elevator is feasible with current-generation fibers because the Moon’s gravity is 1.62 m/s² — one-sixth of Earth’s.

- ISRU market: Valued at $2.6 billion in 2026, projected to reach $5.25 billion by 2030 at a 19% CAGR. This includes terrestrial R&D, simulation, and precursor hardware — the actual in-space revenue comes later.

⚠️ What Could Go Wrong — Phase 1

- Starship V3 delays: If V3 flight testing hits a wall (rapid unscheduled disassembly, pad damage, regulatory hold), the entire downstream timeline shifts. Starlink V3 deployment stalls, HLS testing slips, and orbital compute prototypes are delayed. Starship is the single biggest dependency in this roadmap.

- Orbital refueling proves harder than expected: Starship HLS requires multiple refueling flights in LEO before it can reach the Moon. If propellant transfer at scale doesn’t work reliably, Artemis III/IV slip by years, not months.

- Regulatory capture in orbital compute: If Amazon and legacy telecom successfully slow-roll SpaceX’s FCC approval, the 1M satellite constellation could be delayed 3–5 years. Regulatory risk is underappreciated.

- SLS production bottleneck: There’s one SLS per year planned. If the production line hiccups, Artemis cadence drops. This is why commercial landers (Starship, Blue Moon) are essential — they decouple lunar access from SLS availability.

- China hits its 2030 target first: Not catastrophic, but politically destabilising. If China lands astronauts on the Moon before Artemis IV, expect Congressional panic, possible program restructuring, and ironically, more funding.

Phase 2: 2028–2032 — Establishment

If Phase 1 lays foundations, Phase 2 builds the first permanent structures — on the Moon, in orbit, and in the regulatory landscape. This is the phase where “exploration” becomes “infrastructure.”

Starship: Scaling to Daily Flight

Projected: Starship V4 enters development during this period, targeting 200–300 tonnes to LEO. V4 likely features further-stretched tanks, improved Raptor engines (possibly the Raptor 4 with higher chamber pressure), and refined thermal protection for rapid reuse.

Targeted: SpaceX’s goal is to move from multiple flights per week to multiple flights per day by the early 2030s. This sounds absurd until you do the maths: a fully reusable Starship with a 24-hour turnaround and 2 launch pads can theoretically fly 700+ times per year. SpaceX is building launch infrastructure at Boca Chica, Cape Canaveral, and potentially a sea-based platform to support this cadence.

Projected: Launch cost approaches $100/kg for internal SpaceX payloads (Starlink, orbital compute) by ~2030. External customer pricing will be higher but still revolutionary — maybe $300–500/kg, compared to $2,700/kg on Falcon 9 today. Wright’s Law applies: every doubling of cumulative Starship flights should reduce cost by ~15–20%.

Moon: From Outpost to Base

Targeted: By 2028–2030, the south pole has a permanent outpost — not yet permanently crewed, but with continuous robotic presence and regular crew rotations. Think Antarctic research station, not city.

Projected: ISRU propellant depots become operational by ~2030. Water ice from permanently shadowed craters is extracted, electrolysed into hydrogen and oxygen, and stored as cryogenic propellant. This is the game-changer: once you can refuel on the Moon, the economics of cislunar transport flip. A Starship that refuels at the lunar south pole can reach Mars with significantly more payload than one that launches fully loaded from Earth.

Targeted: 3D-printed habitats and landing pads using regolith sintering are under development by multiple contractors. The concept: use concentrated sunlight or microwave energy to melt lunar regolith into solid structures. No need to launch building materials from Earth — the Moon is the building material. NASA’s ICON and AI SpaceFactory have contracts for this.

In development: Lunar surface transport begins taking shape:

- NASA FLOAT: Flexible Levitation on a Track — a maglev system for moving regolith across the lunar surface. Think of it as a conveyor belt that floats.

- DARPA LunA-10: A programme to design integrated lunar infrastructure, including rail/maglev for hauling processed regolith from mining sites to processing facilities.

In development: Blue Origin’s Blue Alchemist process extracts solar cell material and structural metals directly from lunar regolith using molten regolith electrolysis. If this scales, you can build solar arrays on the Moon from local materials — eliminating the biggest bottleneck for lunar power generation.

Targeted: NASA’s goal is continuous human presence on the Moon by 2032. This means overlapping crew rotations, enough habitat volume for 4–6 people at all times, and ISRU systems reliable enough to support them.

Orbital Compute: The First 100 GW

Projected: xAI and SpaceX are targeting approximately 100 GW of orbital compute capacity by 2030. For reference, the entire current US data center industry consumes roughly 30–40 GW. Putting 100 GW in orbit would more than double global AI compute capacity in one move.

How it works: Each compute satellite carries NPUs powered by solar arrays. The Starlink mesh (by then 20,000–30,000 active satellites) serves as the networking backbone, providing low-latency inter-satellite links and ground connectivity. Workloads are distributed across the constellation, with inference running in orbit and results beamed down.

The economics: At $100/kg launch cost and ~50 kg per compute node, each satellite costs ~$5,000 to launch plus hardware costs. Even at $50,000 per node all-in, 1 million nodes is $50 billion — comparable to what hyperscalers spend on terrestrial data centers annually. The difference: no land acquisition, no grid connection, no cooling costs, no permitting delays. Solar power in orbit is free after hardware cost.

Mars: The First Cargo Ships

Targeted: SpaceX is aiming to send uncrewed Starships to Mars in the October 2028 transfer window. These would be cargo-only missions: supplies, equipment, and test articles for future human missions. The transit time is roughly 6–9 months depending on the trajectory.

Speculative: Elon Musk has stated a goal of the first crewed Mars mission in ~2030 (the next transfer window after 2028). I’ll be direct: I think this is optimistic by 2–4 years. A crewed Mars mission requires proven life support for 2+ years, reliable Starship deep-space operations, and a pre-positioned surface habitat and return propellant infrastructure — all validated by the 2028 cargo missions. If the 2028 missions succeed flawlessly, 2030 is possible. If they encounter significant issues (landing accuracy, power deployment, communication latency operations), we’re looking at 2033 or 2035.

China: Matching Pace

Targeted: China’s crewed lunar landing is scheduled for 2030. If they hit it, they’ll have astronauts on the Moon within 2 years of Artemis IV — possibly before, if Artemis slips.

In development: Tiangong (China’s space station) is planned for multiple expansion modules during this period, growing from the current 3-module configuration to potentially 6 modules. China is also actively recruiting international partners for Tiangong access — a direct counter to ISS partnership politics.

⚠️ What Could Go Wrong — Phase 2

- ISRU doesn’t scale: Lab demonstrations of water ice extraction work. Doing it reliably at tonnes-per-day scale in lunar conditions (temperature swings of ±150 °C, abrasive regolith, vacuum) is a different problem. If ISRU stalls, the entire “refuel on the Moon” strategy collapses, and Mars missions get much more expensive.

- Orbital compute thermal management: Space is a vacuum — you can’t convect heat away. Radiating waste heat from millions of NPUs requires massive radiator surfaces. If thermal limits cap compute density per satellite, the 100 GW target becomes 10 GW, and the economics get harder.

- Mars 2028 cargo missions fail: Mars landing is hard. Historically, the failure rate for Mars missions is ~50%. If SpaceX loses both 2028 cargo ships, the crewed timeline slips to 2033 minimum, and public/investor confidence takes a hit.

- Funding fatigue: The Artemis programme costs ~$4–5 billion/year. US political cycles are 4 years. A new administration in 2029 could redirect funds, slow-roll contracts, or restructure the program entirely. Space programs that depend on government funding are inherently fragile.

- Space debris cascade: As satellite count grows from 10,000 to 50,000+, the probability of collisions increases non-linearly. A single debris-generating event in a busy orbit could trigger a Kessler-like cascade that makes certain orbital altitudes unusable for years. Active debris removal is not yet operational at scale.

Phase 3: 2032–2040 — Industrialization

This is the phase where space stops being an exploration program and becomes an industrial economy. The transition is driven by one core dynamic: it becomes cheaper to make things in space than to launch them from Earth. Not for everything — but for an expanding list of products, starting with propellant and solar cells and eventually including electronics and structural materials.

Moon: The First Off-World Factory

Projected: By the mid-2030s, the lunar south pole base has grown from an outpost to a small industrial settlement. Population: 20–50 people at any given time, with regular crew rotations every 6 months.

Projected: Operational lunar mass drivers — electromagnetic launch rails, sometimes called cargo railguns — come online around 2033–2035. The concept is simple and well-understood physics: accelerate a payload along a rail using electromagnetic force, and launch it off the Moon at escape velocity (2.38 km/s — trivial compared to Earth’s 11.2 km/s). No propellant required. No rocket. No atmospheric friction. Just electricity and a long rail.

A solar-powered mass driver on the Moon could launch thousands of tonnes per year of processed material to lunar orbit, L2, or even Earth orbit at near-zero marginal cost per kilogram. This is the infrastructure that makes lunar manufacturing economically viable — you don’t need rockets to export.

Projected: Self-growing bases become possible as Optimus-class robots (or their successors) handle construction, maintenance, and regolith processing. The human role shifts from construction worker to supervisor and decision-maker. A base with 30 humans and 200 robots can grow faster than one with 100 humans and no robots.

Projected (Casey Handmer’s timeline): Solar array production from lunar materials begins around 2035–2036. Blue Alchemist-derived processes extract silicon, aluminum, and iron from regolith. Solar cells manufactured on the Moon and deployed on the lunar surface or launched to orbit via a mass driver. This is the bootstrap moment — when the Moon starts producing its own power generation capacity from local materials, the growth curve goes exponential.

Projected: High-value exports begin flowing:

- Helium-3: Even modest quantities (100 kg/year) are worth $140 million at current research prices. If fusion power becomes viable, He-3 demand explodes.

- Propellant: Lunar-produced LOX and LH2 delivered to cislunar depots undercuts Earth-launched propellant by 10–50× on cost-per-kg-to-destination.

- Processed metals and solar cells: Launched via mass driver to orbital construction sites.

Speculative: LiftPort’s lunar space elevator concept, if validated, offers a complementary export path — continuous cargo transfer between the surface and a counterweight in lunar orbit, powered by climber vehicles on a tether. Lower throughput than a mass driver, but gentler on cargo and better suited to delicate payloads (humans, fragile electronics, biological samples).

Orbital: The Compute Explosion

Projected: By the mid-2030s, orbital compute capacity reaches 50 million H100-equivalent NPUs. To put that in perspective: as of early 2026, the entire world has roughly 5–10 million H100-class accelerators deployed. Orbital compute could represent a 5–10× expansion of global AI capacity.

Projected: Orbital and lunar AI factories come online — facilities that not only run AI workloads but manufacture their own replacement hardware from space-sourced materials. Moore’s Law meets Wright’s Law meets ISRU: compute gets cheaper because launch gets cheaper because manufacturing moves off Earth because compute gets cheaper. The flywheel spins.

Confirmed (trajectory): The ISS is scheduled for deorbit around 2030–2031. Commercial stations from Axiom Space, Vast, and others are targeted to replace it. By the mid-2030s, commercial orbital habitats host research, manufacturing, and tourism. Low Earth orbit becomes a workplace, not just a destination.

Mars: The First Settlement

Speculative: By the early-to-mid 2030s, the first humans land on Mars — either via SpaceX’s program or potentially a joint NASA-SpaceX mission. The first crew of 10–20 people lands near pre-positioned cargo ships from the 2028 and 2030 windows.

Projected: Early Mars operations focus on:

- Closed-loop life support testing: Can you recycle water and air reliably for 2+ years without resupply?

- Sabatier reaction propellant production: CO₂ (96% of Mars atmosphere) + H₂ → CH₄ + H₂O. This produces methane (Starship’s fuel) and water from local resources. Proven chemistry, but scaling it on Mars with intermittent solar power and dust storms is an engineering challenge.

- Habitat expansion: Initial habs are probably modified Starship hulls. Later structures use Martian regolith for radiation shielding (Mars’s surface radiation is ~0.67 mSv/day, about 100× Earth’s sea-level dose — livable with shielding, dangerous without it).

My honest assessment: Mars settlement in the 2030s will be fragile, expensive, and dependent on Earth resupply for critical components. True self-sufficiency is decades away. But the foothold matters — it proves the concept and identifies the real engineering challenges that can’t be found in simulation.

China: A Second Lunar Power

Targeted: The ILRS base becomes operational around 2035–2036, with robotic systems deployed and initial crewed visits possible. China plans a nuclear reactor on the lunar surface by 2036 — providing reliable, continuous power independent of the 14-day lunar night.

Confirmed (trend): The ILRS partnership has grown to 15+ nations, primarily from the Global South, ASEAN, and the Middle East. China is building an alternative space coalition to the Artemis Accords — and it’s working.

The strategic picture: By the late 2030s, there are two independent lunar presences — US-led (Artemis) at the south pole and China-Russia (ILRS) at a nearby but distinct site. The Moon has geopolitics. This will drive both cooperation (shared safety protocols, communication standards) and competition (resource claims, territorial questions). The Outer Space Treaty of 1967 says you can’t claim sovereignty over celestial bodies. It says nothing about claiming exclusive use of the best ice deposits.

⚠️ What Could Go Wrong — Phase 3

- Mass driver engineering challenges: A lunar mass driver needs to be kilometers long, precisely aligned, and operate in a vacuum with temperature extremes. Construction and maintenance at this scale on the Moon is unprecedented. If mass drivers prove impractical, lunar exports rely on rockets — much more expensive, much lower throughput.

- Lunar dust: Regolith is not like terrestrial soil. It’s electrostatically charged, abrasive, and penetrates everything. Apollo astronauts reported it clogging equipment within days. Long-term industrial operations in lunar dust may require engineering solutions we haven’t invented yet.

- Mars attrition: People will die on Mars. The question is whether the program survives it politically and psychologically. A single catastrophic event (e.g., a hab breach or a medical emergency beyond the program’s treatment capabilities) could set the program back by a decade.

- Orbital debris regulation failure: If international bodies fail to implement binding debris-mitigation rules before constellation sizes reach 100,000+, the collision risk may force costly orbit changes or cap constellation growth.

- Geopolitical conflict on the Moon: Two competing lunar bases near the same resource deposits (south pole water ice) could generate real territorial disputes. The legal framework is inadequate. If this isn’t resolved diplomatically in the 2030s, it becomes a crisis in the 2040s.

Phase 4: 2040–2060 — Maturity & Independence

This phase is the most speculative, and I want to be upfront about that. Predicting 2040–2060 in space is like predicting the internet in 1990 from the vantage point of 1970. The broad strokes are plausible; the specifics will be wildly wrong in ways we can’t anticipate. Still, the trajectory is worth sketching.

The Lunar Industrial Complex

Speculative: By the 2040s, lunar mass drivers are launching 100 million+ units per year into cislunar space — satellites, structural components, solar cell arrays, compute nodes, and propellant packages. The Moon becomes the solar system’s factory floor, and Earth is relieved of the tyranny of its own gravity well for bulk space infrastructure.

Speculative: Lunar factories produce and export:

- Solar arrays for orbital power stations and compute constellations

- NPUs and electronics from lunar-refined silicon and metals

- Structural materials for orbital habitats and Mars-bound cargo

- Propellant to cislunar depots, Mars transit vehicles, and asteroid mining ships

The key economic threshold: when space-produced goods delivered to orbit become cheaper than Earth-launched equivalents. For bulk commodities (metals, propellant, solar cells), this crossing point is projected somewhere in the 2035–2045 range, depending on mass driver throughput and lunar manufacturing yield. Once crossed, it triggers a self-reinforcing cycle — more orbital demand drives more lunar production, which drives lower costs, which in turn drives more demand.

The AI Flywheel

Speculative: This is the dynamic that could make the 2040s and 2050s feel like science fiction:

Orbital and lunar compute capacity reaches terawatt scale. AI systems — running on space-manufactured NPUs, powered by space-manufactured solar arrays, launched by lunar mass drivers — are designing, optimizing, and controlling the manufacture of more compute. Compute builds more compute. The growth rate is limited not by engineering talent or capital, but by the speed of raw material processing and energy collection.

This is what I called the “frontier of independence” in Part 1. The space economy no longer depends on Earth for its growth inputs. Earth provides people, intellectual property, and high-complexity components. Space provides energy, raw materials, and bulk manufacturing. The relationship becomes complementary rather than dependent.

Mars: Toward Self-Sufficiency

Speculative: The Mars settlement grows through the 2030s and 2040s, with population reaching hundreds by 2040 and potentially thousands by 2050. The self-sustaining city timeline — where Mars could survive indefinitely without Earth resupply — is probably 2045–2055, and even that assumes aggressive development of technologies for closed-loop agriculture, local manufacturing, and medical self-sufficiency.

The hardest problems for Mars self-sufficiency aren’t engineering — they’re biological and social. Can you grow enough food in Martian soil with Martian sunlight (~590 W/m² at Mars orbit, vs ~1,361 W/m²** at Earth)? Can you maintain genetic diversity with a population of thousands? Can you build a functional society 225 million km from Earth with a 4–24 minute communication delay? These are open questions.

Projected: Lunar-produced propellant and components significantly reduce Mars mission costs. A Starship refueling at a cislunar depot with lunar-produced propellant, carrying lunar-manufactured cargo, costs a fraction of an all-Earth-launched equivalent. The Moon doesn’t just enable the Moon — it enables Mars.

The Asteroid Frontier

Speculative: Asteroid mining operations begin in the 2040s, initially targeting near-Earth asteroids (NEAs) for platinum-group metals and water. A single 500-meter metallic asteroid contains more platinum than has ever been mined on Earth. The challenge is the delta-v budget and the round-trip time.

Lunar mass drivers and cislunar propellant depots change the asteroid equation. A mining ship that launches from lunar orbit with lunar propellant has a much lower energy budget than one launching from Earth’s surface. The Moon is the staging ground for the asteroid economy.

The Outer Solar System

Speculative: Jupiter’s moons — particularly Europa (subsurface ocean, potential astrobiology) and Ganymede (magnetic field, water ice, radiation shielding potential) — become targets for robotic exploration in the 2040s and potentially human missions in the 2050s. This is at the far edge of plausibility for this timeline, but the infrastructure built for Moon and Mars (reliable nuclear power, closed-loop life support, autonomous robotics) applies directly.

The Cislunar Economy

Speculative: By 2060, the space economy is measured in trillions of dollars annually. For reference, Morgan Stanley projects the space economy will reach $1.8 trillion by 2040 (from ~$469 billion in 2024). I think that estimate is conservative if launch costs and ISRU hit their targets, and wildly optimistic if they don’t. The variance is enormous.

The economic composition shifts over time:

- 2026–2035: Dominated by launch services, satellite communications, and government contracts

- 2035–2045: ISRU products, orbital compute services, and lunar manufacturing grow rapidly

- 2045–2060: Space-to-space economy (lunar exports to Mars, asteroid resources to orbital facilities) becomes larger than the space-to-Earth economy

⚠️ What Could Go Wrong — Phase 4

- The bootstrap never happens: If lunar manufacturing can’t achieve competitive costs vs Earth launch, the entire industrialization thesis collapses. Space remains a government-funded exploration program, not an economy. This is the existential risk for the whole roadmap.

- Energy storage, not generation, is the bottleneck: Solar power in space and on the Moon is abundant, but storing it through the 14-day lunar night or transmitting it to Mars requires battery or beamed-power technology that may not scale as projected.

- Political collapse of space programs: A major war, economic depression, or a political movement against space spending could defund Artemis and reduce NASA to a shadow of its former self. SpaceX can survive on Starlink revenue, but the broader ecosystem depends on government anchor customers.

- Biological limits: Long-duration spaceflight effects (bone loss, radiation, psychological stress) may prove harder to mitigate than assumed. If humans can’t live healthily on the Moon or Mars for years at a time, the settlement timeline would be dramatically extended.

- We’re wrong about something fundamental: Every long-range forecast has unknown unknowns. Maybe ISRU chemistry has a scaling wall we haven’t hit yet. Maybe orbital debris makes LEO unusable. Maybe AI development plateaus, and the compute demand thesis evaporates. Humility about our own ignorance is the most honest position.

The Confidence Gradient

Here’s my honest confidence level for each phase:

- Phase 1 (2026–2028): High confidence (75–85%). Most of the hardware exists. Artemis II is done. Starship V3 is in final testing. The pieces are real. The question is timing, not feasibility.

- Phase 2 (2028–2032): Moderate confidence (50–65%). Depends heavily on Phase 1 execution. ISRU at scale is unproven. Mars cargo missions are high-risk. But the trajectory is clear and funded.

- Phase 3 (2032–2040): Lower confidence (30–50%). Industrial lunar operations are technically plausible but have never been attempted. Mass drivers are proven physics, but unproven engineering at this scale. Many things need to go right simultaneously.

- Phase 4 (2040–2060): Speculative (15–30%). The broad direction is plausible. The specifics are almost certainly wrong. I’d bet on something like this happening, but the actual timeline could be 10–20 years later than projected. Or 10 years earlier, if AI acceleration surprises us.

The Overarching Pattern

Zoom out, and the pattern across all four phases is the same: reduce the cost of moving mass, then use that to build infrastructure that further reduces cost. It’s Wright’s Law applied to civilization-scale engineering.

- Starship reduces launch cost by 10–100× → enables mass satellite deployment

- Starlink generates revenue → funds Starship development → funds lunar missions

- Lunar ISRU produces propellant and materials locally → reduces cost of everything in cislunar space

- Mass drivers eliminate propellant cost for lunar exports → makes space manufacturing competitive with Earth

- Orbital compute generates revenue from space-based AI → funds constellation expansion → funds more compute

Each link in the chain enables the next. Break any one link, and the downstream timeline slows dramatically. Strengthen any one link, and everything accelerates.

This is why I keep coming back to the concept of the frontier of independence — the point where space infrastructure can grow without being bottlenecked by Earth launch capacity. We’re not there yet. Phases 1 and 2 are about getting there. Phases 3 and 4 are about what happens after.

What I Got Wrong (A Pre-emptive Section)

In five years, I’ll look back at this timeline and wince at specific predictions. Some things I suspect I’m wrong about:

- I’m probably too optimistic about ISRU timelines. Water ice extraction sounds simple. Doing it at scale, in permanent shadow, at -230 °C, with equipment that can’t be easily repaired, will be harder than anyone’s PowerPoint suggests.

- I’m probably too pessimistic about AI acceleration. If AI capabilities continue their current trajectory, autonomous construction and manufacturing could arrive faster than I’ve projected, compressing Phase 3 by several years.

- I’m probably wrong about Mars crew timelines. Musk says 2030. I say 2033–2035. Reality might be 2032 or 2037. The variance is wide.

- I haven’t accounted for black swans. A breakthrough in fusion power changes the energy economics. A space debris cascade changes the orbital economics. A geopolitical crisis changes the funding economics. The timeline assumes no major discontinuities — and discontinuities are exactly what’s most likely over a 34-year span.

I hope the future surprises me and lets me learn.

Summary: The Living Roadmap

- 2026–2028: Starship V3 flies. Artemis puts humans on the Moon. Orbital compute prototypes launch. China begins ILRS construction. The foundations are poured.

- 2028–2032: Lunar base grows. ISRU begins producing propellant. First cargo ships reach Mars. Orbital compute scales to 100 GW. Continuous lunar presence achieved.

- 2032–2040: Mass drivers export lunar products. Factories on the Moon produce solar cells and electronics. Mars settlement begins. AI flywheel activates. Two competing lunar presences operate.

- 2040–2060: Space economy reaches trillions. Mars pushes toward self-sufficiency. Asteroid mining begins. Lunar factories supply the solar system. The frontier of independence is crossed.

This roadmap will be wrong in its details. But I believe the direction is right, and the underlying physics and economics are sound. The question is when, and who leads.

Next in the series: Part 3 — Payload Economics: How Starship Changes Everything → — the real numbers behind $/kg to LEO, the $90M Voyager contract, orbital refuelling, and why Wright’s Law means costs keep falling.